Reflections on the Downgrades by the Ratings Agencies

This brief is a summary of the most recent decisions taken by the credit ratings agencies on South Africa's credit rating following the cabinet reshuffle in March this year. Standard and Poor's and Fitch downgraded the countries foreign currencies to non-investment grade, while Moody's has put the country's sovereign ratings on review for downgrade. The economic implications of the downgrade are evaluated

Introduction

The recent cabinet reshuffle has raised serious concerns related to the level of risks associated with investment confidence and political stability. This led to the decisions by the three major international credit ratings agencies, Standard & Poor’s (S&P), Moody’s and Fitch, to review the credit ratings of South Africa. S&P and Fitch downgraded the country’s foreign currency rating to non-investment grade (commonly referred to as “junk status”). Moody’s has put South Africa’s sovereign rating on review for a downgrade. This brief summarises the most recent decisions taken by the three ratings agencies and comments on some of the implications.

Overview

Both quantitative and qualitative factors are taken into account in determining sovereign credit ratings. The overriding criteria which typically govern a rating are the following general considerations: the expected economic growth of an economy, its resilience to potential shocks, the quality and predictability of a government’s decision-making, whether the state’s debt position is manageable and whether the state is able to balance its expenses as against its revenue.

“Investment-grade” is a term broadly used to describe governments with relatively high levels of creditworthiness and credit quality. In contrast, the term “speculative” or “non-investment grade” (or “junk status”) generally refers to governments which may currently have the ability to repay but face significant uncertainties that could affect credit risk.

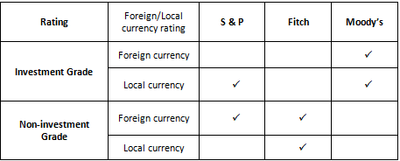

Since the respective ratings by the agencies may seem somewhat confusing at first sight (as they use different symbols to denote the different levels) the following table provides a simplified overview of the current status , reflecting the long-term foreign and local currency ratings (the same levels are reflected in the respective short-term ratings).

Standard and Poor’s

On 3 April 2017, S&P announced its decision to lower the long-term foreign currency sovereign credit of South Africa from BBB- (the lowest investment grade) to BB+ (the highest non-investment grade) and the long-term local currency rating from BBB to BBB- (therefore still in investment grade, but on the lowest level). A negative outlook was assigned to all long-term ratings.

S&P’s rating action reflects the view that the recent cabinet reshuffle has put policy continuity at risk and has increased the likelihood that economic growth and fiscal outcomes could be negatively affected. It believes that the contingent liabilities of public enterprises, especially in the energy sector will rise. Rising political tensions could delay structural reforms and reduce investor confidence. This could lead to currency depreciation and an increase in real interest rates. The current account deficit is expected to average close to 4% of GDP in 2017-2020 and inflation is expected to fall below 6% this year and to remain within the inflation target of 3%-6% over the next three years. The negative outlook is an indication that political risks will remain elevated, and fiscal and economic outcomes are likely to be negatively affected as a result of policy shifts.

Moody’s

On 3 April, Moody’s announced that it had placed the long-term ratings of South Africa on review for a downgrade. Although it has acknowledged that changes in a ministerial cabinet do not automatically lead to material changes in a country’s credit profile, Moody’s decision reflects a view that the cabinet reshuffle raises questions on the prospects for ongoing reforms, the underlying strength of South Africa's institutional framework, and the fragile recovery in the country's economic and fiscal position. During the review, Moody’s intends to assess, inter alia:

The possibility of changes in key areas of financial and macro-economic policy making, as well as in strategic areas such as energy policy.

Any likely changes in the government's plans and the implications for potential growth and for the reversal of the rising debt burden.

Any implications for progress on currently stalled structural reforms in strategic areas such as regulation of the mining sector or regulations that would increase transparency in the financial transactions of large businesses; and the prospects for continued progress on reforms to enhance transparency, accountability and good governance in the SOE sector, and to remove structures that encourage rent-seeking over achievement of public policy goals.

The implications of the underlying political dynamics which led to the cabinet reshuffle for the predictability of South Africa's institutional framework, including for the government's capacity to conduct sound economic policies which foster economic and fiscal strength.

Whether the ongoing tensions within the ANC weaken the credibility and effectiveness of South Africa's policymaking, the effectiveness and independence of the public service and ultimately the strength of the country's institutions.

Fitch

On 7 April 2017, South Africa’s long-term foreign and local currency ratings were downgraded to non-investment grade by Fitch (from BBB- to BB+), with a stable outlook. The rating action reflects the view that the cabinet reshuffle will undermine standards of governance, as well as public finances.

According to Fitch, this could lead to:

A change in the direction of economic policy.

A weakening of the progress of governance of state-owned enterprises, raising the risk that this could put pressure on the government’s budget.

Upward pressure on general Government debt. Although the newly appointed Finance minister does not intend to change fiscal policy and remains committed to expenditure ceilings, fiscal consolidation will be less important given the recent focus on radical socioeconomic transformation. It is unlikely that a fall in revenue as a result of slow GDP growth than expected will be compensated by expenditure measures, and this could raise general government debt estimated at 53% of GDP in March 2017.

In addition, Fitch believes that tensions within the ANC could weaken Treasury’s ability to resist departmental demands for increased spending. Political uncertainty has been an important factor behind slow growth last year and the recent cabinet reshuffle will negatively affect the investment climate even further. GDP growth is expected to be 1.2% in 2017 and 2.1 % in 2018.

Economic implications of a downgrade

Investors around the world rely on credit ratings. Quite apart from providing guidance for investing or business decisions in general, some international asset managers and lenders are not allowed to invest or to provide funding to countries or companies that do not have appropriate credit rating by one (or more) of the three major ratings agencies.

The first direct impact of a sovereign downgrade is normally seen as an increase in a government’s borrowing rate. The Governor of the South African Reserve Bank put it as follows on 11 April 2017:

When you lose your investment grade rating, your government is going to pay more to raise debt and when your government does that your banks are going to pay more to raise debt and they will pass those costs to businesses and households and then it doesn’t become nice… It’s going to affect the poor and the middle class who rely on credit.

A secondary impact will be on a country’s currency as it would tend to weaken in these circumstances. Whilst the Rand has already been affected in this regard, a further depreciation is to be expected over the longer term. In this context, it needs to be pointed out that whilst Fitch has downgraded South Africa in respect of both local and foreign currency and Moody’s has placed the country on review for a downgrade, S&P’s downgrade relates only to foreign currency and leaves the local currency on the lowest rung of investment grade. This is important, since, as S&P itself points out, whilst only 10% of government’s debt stock is denominated in foreign currency, non-residents also hold about 35% of the government’s Rand-denominated debt.

The latter holding would be affected by any future downgrade in the local currency rating, also since much of the 35% is most probably held by asset managers who are not permitted to invest in non-investment grade assets. The proceeds of any large-scale sale of this 35% would flow out of the country and would put substantial further pressure on the Rand’s value. The market reaction so far (however dramatic it may seem), can therefore be seen as only the beginning of a process, if further downgrades follow. Further depreciation will add to the inflation rate, increasing pressure on the SA Reserve Bank to raise interest rates (or at the very least, not to lower them).

It may seem counter-intuitive, but the fact that the overall JSE index has risen in these circumstances, actually further reinforces the market perception on the future value of the currency. This is so, since a large part of the value on the JSE relates to companies whose activities generate foreign currency revenues.

The effect of an increase in Government’s borrowing costs will make less funding available for Government spending, particularly when annual economic growth is well under 1% as at present (in other words, Government’s debt service costs rise faster than revenue). Government needs to borrow in order to fund its expenses and any increase in Government’s debt service costs will inevitably put pressure on Government spending in general (the share of debt service in the central Government budget is already at 11% of total expenditure).

This will place pressure on many areas of Government expenditure, such as education and training, human settlement; health and social protection, which together make up 56% of current Government spending. It is to be expected that the cost of funding for banks will also increase, and such increased costs will obviously flow through to borrowers, increasing the cost of consumer and business debt.

Experience has shown that it can take many years for a country to recover from a downgrade to non-investment status and to regain investment status. An analysis by Moody’s investor service of moves between sovereign rating categories over the period 1983-2010 found that the average annual probability of moving between Ba (highest “junk status” category) and Baa or better (investment grade categories) was 7.51%. This implies that a country rated Ba would on average take more than 13 years to move upwards. Moreover, there was a 6.04% annual probabilities that there would be a downward movement from Ba status (see Moody’s report, entitled "Sovereign Debt and Recovery Rates, 1983 - 2010").

Conclusion

Quite apart from the initial shock, the longer term effect of downgrades is negative. They have already provided a blow to business and investor confidence. It is expected that as a consequence, this will lead to lower (or stagnating) economic growth and fewer new jobs being created. The poor and disadvantaged sections of society will be the first to suffer the consequences.

Agathe Fonkam is a Researcher at the Helen Suzman Foundation.

This article first appeared as an HSF Brief.