Missing salaries or lost jobs – the crisis deepens in June 2020!

29 July 2020

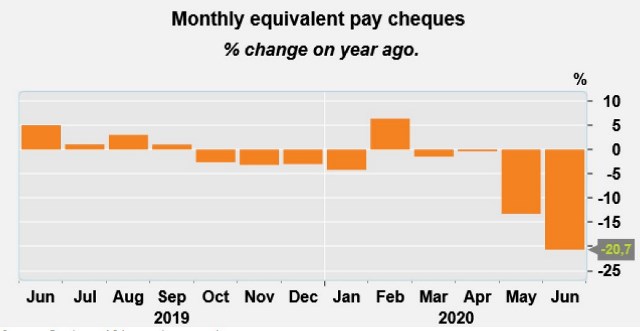

The number of take-home monthly payments in June 2020 decreased by -20.7% on a year ago. The crisis stemming from the COVID-19 lockdown levels and its impact on the economy, has affected a fifth of employees’ salaries that gets processed by BankservAfrica through the South African National Payment System.

As the BankservAfrica Take-home Index (BTPI) records the majority of payments from large corporates and a fair number of medium-sized firms that are served by payroll service providers and firm-owned payroll administrators, the recent decrease may not reflect the full impact of salary declines on small firms. However, with the BTPI over representing the majority of payments from civil servant and state-owned entity payrolls, it becomes evident that the reduced salary numbers are most likely to be in the private sector. This is supported by data showing an estimated 30% of the BTPI monthly equivalent payments are paid by the broader government sector compared to 21% shown in Stats SA’s Quarterly Employment Survey.

It is possible that a fifth of employees in the private sector did not receive a salary in June 2020. The -20.7% decline could be the result of job losses or it could due to a temporary pause in payments. We caution that while our salary data cannot be used as a measure of the unemployment rate, it can, in this very unusual time, provide a quick and effective indication of the employment statistics on the ground through the number of salaries paid.

From our data, we can confirm that overall employees received reduced salaries compared to a year ago and that less employees were paid (however, the movements may also be due to some late UIF payments). This strongly suggests tougher times for employees and their ability to spend.

The actual average take-home pay declined by -0.5% in real terms. This could have been the result of instances where salaries may have increased or that the personal income tax provided relief above the current inflation rate.

As the average tax relief of over 5.1%, an increase of 4% in gross salaries on average would have resulted in a 4.2% increase due to this reduction in income tax. Therefore, the 1.7% increase (as reflected in the nominal year on year change in the BTPI) is extremely low. Moreover, when inflation declines, as it currently has, real take- home pay increases at a faster rate – it does not decline as it did in June.

BankservAfrica and economists.co.za have created an estimate of the number of payments for each salary category and their annual movements. This is based on the amount of salaries paid and BankservAfrica’s numbers of how often these payments took place.

Table 1: Estimates of the number of payments that declined by salary category

|

Type of payment description |

% change from June 2019 |

|

Number of overall take-home payments (monthly equivalent) |

-20.7% |

|

Daily / Casual payments |

-35.2% |

|

Weekly payments |

-17.1%% |

|

Monthly payments |

-9.1% |

Actual monthly nominal and real take-home salaries recorded for June

The seasonally adjusted nominal take-home salary in June was R15 869, which was 1.7% higher than in June 2019. The real monthly take-home pay was R14 197. The real take-home pay declined by -0.5% on an estimated inflation rate of 2.4% in June 2020.

The BankservAfrica Private Pension Index (BPPI) declined for the second consecutive month, falling by -0.3% to reach R7 355 in real terms. Real pensions could be declining as a result of the interest rate falls and as other assets have also struggled.

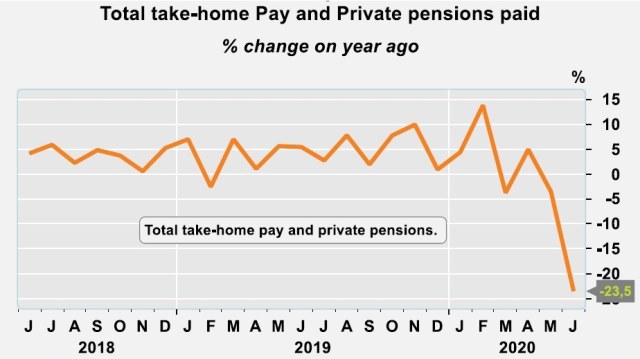

The total value of take-home salaries paid in June declined by -25.6% while total pensions paid dropped by -4.6% both in nominal terms. The combined decline for total take-home pay and pensions was by far the biggest on record at -23.5%!

The numbers are concerning and will have a profound impact on the South African economy. The knock-on impact is also likely to be larger than many have estimated and will have a severe impact on retail sales and consumer spending.

Graph 1: Annual % change of take-home pay vs private pensions in June 2020

Source: BankservAfrica and economists.co.za (note: the dotted line represents the inflaton forecast)

Graph 2: Monthly % change of take-home pay for 2020 and 2019

Source: BankservAfrica and economists.co.za

Table 2: The BankservAfrica Take-home Pay Index data

|

Month |

Nominal average take- home pay |

Real take- home pay |

Nominal BTPI % change YoY |

Real BTPI % change YoY |

Nominal average pensions paid |

Real private pension |

Nominal BPPI % change YoY |

Real BPPI % change YoY |

|

Jan-19 |

15090 |

13588 |

1,2% |

-3,2% |

7498 |

6848 |

6,5% |

2,0% |

|

Feb-19 |

15353 |

13718 |

1,5% |

-2,5% |

7646 |

7031 |

7,9% |

3,7% |

|

Mar-19 |

15321 |

14098 |

3,8% |

-0,3% |

7578 |

6978 |

6,3% |

2,2% |

|

Apr-19 |

15237 |

14176 |

4,6% |

0,3% |

7801 |

7189 |

9,9% |

5,2% |

|

May-19 |

14965 |

14117 |

5,1% |

0,6% |

7846 |

7211 |

10,1% |

5,5% |

|

Jun-19 |

15598 |

14272 |

3,0% |

-1,3% |

8428 |

7374 |

10,3% |

5,6% |

|

Jul-19 |

16326 |

14599 |

2,4% |

-1,7% |

8237 |

7204 |

7,5% |

2,9% |

|

Aug-19 |

17538 |

15259 |

3,5% |

-0,8% |

8211 |

7205 |

7,5% |

3,4% |

|

Sep-19 |

17250 |

14869 |

3,8% |

-0,3% |

8251 |

7234 |

8,3% |

3,8% |

|

Oct-19 |

16692 |

14585 |

6,5% |

2,3% |

8277 |

7260 |

8,5% |

4,2% |

|

Nov-19 |

16177 |

14324 |

8,8% |

4,9% |

8052 |

7073 |

7,4% |

3,6% |

|

Dec-19 |

16052 |

14164 |

9,6% |

5,7% |

8098 |

7116 |

7,6% |

3,9% |

|

Jan-20 |

16502 |

14297 |

9,4% |

5,2% |

8060 |

7077 |

7,5% |

3,3% |

|

Feb-20 |

16505 |

14128 |

7,5% |

3,0% |

8286 |

7292 |

8,4% |

3,7% |

|

Mar-20 |

16107 |

14161 |

5,1% |

0,4% |

8247 |

7257 |

8,8% |

4,0% |

|

Apr-20 |

15703 |

14042 |

3,1% |

-0,9% |

8153 |

7214 |

4,5% |

0,4% |

|

May-20 |

15506 |

14192 |

3,6% |

0,5% |

7970 |

7115 |

1,6% |

-1,3% |

|

Jun-20 |

15869 |

14197 |

1,7% |

-0,5% |

8579 |

7355 |

1,8% |

-0,3% |

Note on Table 1: Estimates of the number of payments that declined by salary category

Payments data from the BankservAfrica payroll database system were used to determine the estimate number of payment declines per salary category. Weekly payments were adjusted in line with the number of Fridays, Thursday and Mondays in a month. For daily payments, our adjustments are adjusted for the number of weekdays when these payments typically take place. This methodology ensures we compare with like.

About BankservAfrica

BankservAfrica is the trusted payments partner and Financial Markets Infrastructure (FMI) to the financial services industry. As the largest automated payments clearing house in Africa we clear and process billions of low value card, ATM and EFT transactions annually. Our role in the South African National Payments System (NPS) is to facilitate interoperability between the banks and ensure regulatory compliance with our regulators against international banking security best practice and standards and reduces risk and complexity in the industry.

We continue to strive to be a world class and pre-eminent payments operator, innovator and payments partner of choice in Africa, by simplifying our worlds through combining trusted transactions with sensitive information.

BankservAfrica’s national responsibility is to provide safe financial payment services for 56.7 million South Africans,

irrespective of their location in partnership with our shareholders and partners.

With a 48-year history in South Africa, BankservAfrica operates 24/7, 365 days a year and delivers on very strong SLAs.

Issued by BankservAfrica, 29 July 2020