Wealth Taxes 1: Conceptual Framework

4 April 2018

Introduction

The debate around wealth taxes has gathered steam globally as the gap between the rich and poor continues to grow. This brief provides descriptions of the most pertinent concepts involved.

The difference between wealth and income

Wealth is what one owns at a specific point in time and is measured as assets less liabilities. Income is defined as the inflow of cash one earns over a specific period (usually a tax year) and comes in the form of a salary, wages, profit, interest, endowment income, rent, etc.

The various forms of wealth

Wealth comes in various forms: real estate, financial assets, business assets, pension entitlements, trust assets, objects of value and so forth. This matters because wealth taxes may be based on only some forms of wealth, or they may treat different forms of wealth differently.

The difference between tax on wealth, tax on wealth transfers, tax on income from wealth and capital gains tax

A wealth tax is an annual tax levied against the market value of net assets (assets less their associated liabilities) owned by taxpayers. It can be levied against both natural and juristic persons.

A wealth transfer tax is levied on the passing of ownership of assets from one person (or entity) to another. It is imposed where there is a legal requirement for registration of the transfer, such as transfers of real estate, shares, or bonds. Examples include inheritance tax, gift tax, transfer duty and securities transfer tax (STT).

Tax on income from wealth includes taxes on dividends and net interest (interest income less interest expense) and rental income.

Capital gains tax (CGT) arises when an asset is disposed of and the proceeds exceed the asset’s original cost. For purposes of wealth tax analysis, CGT forms part of income tax.

The difference between annual wealth taxes and a capital levy

Compared to a wealth tax, a capital levy a one-off tax on private wealth and has historically been used as an exceptional measure in an attempt to restore debt sustainability by retiring public debt.

The forms of taxes on wealth and wealth transfers

Estate duty

Estate duty is levied against the estate of a deceased individual before the transfer of any estate assets.

Transfer duty

Transfer duty is a tax levied on the value of any real property acquired by any person by way of a transaction or in any other way.

Donations tax

Donations tax is levied on the value of assets transferred by donation. It is most often levied against the donor but if the donor fails to pay the, the donee may become liable. Donations are the form of wealth transfer are likely to be tax deductible.

Gift tax

Gift tax is levied on the value of assets transferred by an individual (during his/her lifetime/inter vivo) or entity to another individual or entity (excluding charities). The individual or entity making the transfer receives either no remuneration or remuneration below the asset’s market value. Gift tax can be levied against the person or entity giving the gift or the receiver of the gift. Gifts are generally taxed at a higher rate than donations and less likely to be tax deductible.

Property rates

Property rates are levied on the value of the real property which includes land, buildings or other immovable improvements to the land which increase the value of the real estate. The tax is often assessed by local or municipal governments and mainly used by municipalities for repairing roads, building schools, or other similar services.

Taxes based on an annual return on assets

Taxes based on an annual return on taxes are levied on any unrealised net asset returns for the financial year. Asset returns that are realised are levied as CGT.

Inheritance or estate tax

Inheritance or estate tax is levied on the value of assets transferred by an individual upon death (testamentary transfer) via his/her estate to another individual or entity (excluding charities). Inheritance tax can be levied against the estate or the heir.

When any of the above taxes are applied, the revenue authorities take into account their country’s unique circumstances and these result in differences rates and concessions between countries.

***

Wealth Taxes II: Rationales

Introduction

This brief discusses the rationales for wealth tax, eight in total; reducing inequality, a source of funding, the views of Thomas Piketty, improved horizontal and vertical tax equity, reducing tax avoidance, encouraging efficient resource use, capital levies for special purposes and finally politics and history.

Reducing inequality

Excessive inequality leads to political polarization and lower economic growth. Inequality impairs productivity when those with low incomes suffer poor health or struggle to finance their education. It further damages growth when politicians exploit political polarization to abandon sometimes unpopular yet growth friendly economic policies.

Inequality can be viewed from different but related perspectives: inequality of income, inequality of wealth, lifetime inequality (income over a lifetime) and inequality of opportunity. All these concepts offer different yet complementary insights, providing better guidance to government policies aimed at addressing inequality [1].

Over the past three decades, 53 per cent of countries globally have seen an increase in income inequality [2] and a growing concentration of wealth has been reported in several advanced economies after many decades of equalization. [3] Wealth is very unequally distributed – even more so than income: in advanced economies, the top 10 percent own, on average, more than half the wealth. [4]

Assessments of the effect of tax measures on inequality are scarce. [5] That said, a comprehensive case study on Sweden and Germany entitled An Annual Wealth Tax published in 1975 by Cedric Sandford, a former professor of political economy at Bath University, concluded that the since abandoned wealth taxes in these countries were ineffective at reducing inequality. A far more recent study on France, published in 2010, found that despite the existence of a wealth tax there, inequality has kept growing. [6]

From an income perspective, Scandinavian countries are amongst the most equal societies in the world. Yet Denmark, Finland and Sweden no longer impose wealth taxes, leaving only Norway and Iceland with them still in place. The reasons for the enviable levels of equality in these countries seems most likely to be the population’s buy-in to social democracy, as well as effective centralized bargaining by trade unions [7] that represent around 70 percent of the total workforce for most these countries. [8]

A source of funding

Designing a broad tax base that provides stable and sustainable sources of revenue with minimal economic distortion is a central policy objective of tax authorities worldwide. While the objective may be a perennial one, it moved to the forefront of debate during the recent financial crisis when the sensitivity of some streams of government revenue to economic fluctuations became apparent at the same time as unprecedented demands were being made on expenditures. As a result, wealth taxes were re-introduced in Spain and Iceland in an attempt to raise revenue. [9]

In emerging markets the following factors pose additional risks to the fiscus:

1. There has been heightened financial volatility and downward revisions of potential growth, [10] while a 1 percent decline in growth in emerging markets would on average result in a 0.3 percent of GDP deterioration in their fiscal balances.

2. Estimates based on a sample of nine emerging market economies representing a cross-section of commodity exporters suggest that a 10 percent across-the-board fall in commodity prices would lead to a decline of more than 1 percent of GDP in budget revenues annually.

3. Interest rate risks have increased due to potential sovereign debt rating downgrades and uncertainty around US interest rates. In the event of rating downgrades or a sudden rise in US interest rates, gross financing needs could increase sharply, particularly where the domestic investor base would be unwilling or unable to increase their holdings of government bonds.

4. Contingent liabilities of state-owned enterprises too are a source of vulnerability (for example in China and South Africa). [11]

What makes the wealth tax appealing from a revenue perspective is a very large tax base. This leads proponents to believe that relatively low tax rates are sufficient to generate a substantial amount of revenue. As wealth is considerably more concentrated than income, the percentage of households liable for a recurrent wealth tax could be kept small and the rate low resulting in considerable revenue - at least in theory and assuming limited changes in behavior. [12]

Thomas Piketty

Thomas Piketty is a French economist whose work focuses on wealth and income inequality. Piketty is the author of the best-selling book Capital in the Twenty-First Century (2013), which emphasises wealth concentration and distribution over the past 250 years. Piketty is currently the most influential proponent of a progressive wealth tax.

Piketty believes that wealth tax will play an important role in public finance debates for decades to come because of at least two reasons: one theoretical and another empirical. Existing theories of optimal labour income taxation offer a useful basis for informed policy discussion but nothing close to this exists for theories of optimal capital taxation. Second, and maybe more importantly, in most OECD countries, aggregate household wealth to household income ratios have increased substantially since the 1970s, with an acceleration of the trend since the 1990s. This is due to rising asset prices (property and share prices) as well as a long-term recovery in countries strongly hit by the century’s world wars.

In theory, an increase in the capital/income ratio should push the tax mix in the direction of greater reliance on capital taxation. Piketty notes however that it would be misleading to make such predictions because historical experience suggests that the political economy of capital taxation involves complex, country specific and quantitatively important issues. [13]

Referring to a principle underpinning a number of property taxes, Piketty suggests that wealthier individuals benefit more from the protection of property rights enforced by government and therefore should contribute more to the costs associated with upholding these rights. [14]

In his earlier writings, Piketty posits that by the commitment of pledgeability, asset ownership is an important prerequisite to the access of credit: by easing funding constraints for less wealthy sub-populations, a more equitable distribution of assets might release entrepreneurship and innovation, and improve growth. [15] Some would argue that wealth taxes are a way of achieving a more equitable distribution of assets.

Piketty’s most radical proposal is a global tax on wealth. He admits that the idea is “utopian” but shouldn’t be beyond political imagination in the need for bold, dramatic efforts to combat inequality. [16] He argues that it may be made possible by the recent “revolution” in information exchange between countries - including moving toward global, automatic exchange of information.

Improving horizontal and vertical tax equity

Horizontal equity means those with the same ability to pay taxes should be taxed the same. Assume two individuals receive the same income but only one of them holds assets. The person holding assets is seen as having greater ability to pay taxes.

In cases of inherited wealth, consider a world where individuals are born with the same initial wealth (if any) and differ only in productivity. As they grow older their wealth will differ due to past labour income. In such a world, a well designed tax on labour income is sufficient and taxing wealth is just an indirect way of taxing past earnings. Now consider individuals with identical productivity but different levels of initial or inherited wealth. It is no longer true that a tax on labour income is sufficient. [17]

In a welfarist framework, the normative yardstick of tax design is individual utility and wealth is a source of utility in its own right. This includes power and command over resources, providing an advantage in bargaining situations, resulting in over-proportional political influence and rent-seeking. [18]

Vertical equity is based on the idea that those who earn more money, or have more economic resources, should be taxed at higher rates than those earning less. This idea underpins progressive income tax and is the most common income tax system globally. However, tax systems around the world have become steadily less progressive since the early 1980s. They now rely more on indirect taxes (on goods and services), which are generally less progressive than direct taxes (against corporate and personal income), reflecting most notably steep cuts in top marginal rates. [19] Taxes on capital income too are now often imposed at low effective rates or evaded. [20] Furthermore, since 2000 the labour share of income has fallen and forward technological progress might accelerate this trend through the substitution on capital for labour. So while the restoration of more progressive income taxation could contribute to a fairer distribution of tax burdens, some argue that such systems will need to be complemented with asset-based systems such as wealth tax. [21]

Wealth tax systems themselves can and have been progressive according to the amount of wealth, as advocated by Piketty.

Reducing tax avoidance

Two popular theories for using wealth tax to reduce general tax avoidance are:

a. As assets are declared, these can be used to cross-check income tax returns as there should be a close correlation between wealth in assets and income.

b. Annual asset declarations required by a wealth tax will help detect when owners do not execute a traditional sale when disposing of an asset in order to avoid paying capital gains tax.

I have found no material evidence of the above occurring in practice.

A less frequent argument for wealth tax in this regard was put forward recently by Martin Weale, a Professor of Economics at King's College London and former Director of the National Institute of Economic and Social Research in the UK. Weale argues that if income can be easily dressed up at capital gains and the latter cannot be taxed as income, as is perhaps the case in the UK, there may be a case for a wealth tax.

Encouraging efficient resource use

Proponents argue that a wealth tax enhances economic efficiency because it induces to taxpayers to use their assets more efficiently to pay the tax or otherwise sell them to someone that can. Under this theory, investment would increase and the economy will grow faster.

From an economic perspective, the argument seems peculiar because the theory rests on the assumption that individuals are naïve and ignorant when making their investment decisions in a tax free world. Only if government puts additional pressures on taxpayers by claiming part of their wealth, the argument goes, will they be motivated to look for more profitable investment opportunities. [22]

Gabriel Zucman, an economics professor at the University of Berkley and a frequent collaborator with Piketty, does not envision that the wealth tax will have a meaningful effect on growth or investment. Zucman states that “There really isn’t any good empirical study on this question,” and “In theory, it can go in any direction. It could increase savings and investment or it could decrease savings and investment.” [23]

Capital levies for special purposes

The difference between a capital levy and wealth tax is that a capital levy is once off.

The sharp deterioration of public finances in many countries post the financial crisis has revived interest in a capital levy on private wealth to try and restore macro-financial stability/debt sustainability. Crisis-driven adjustments have tended to burden those with incomes from labour more heavily in the form of income tax surcharges. As such, some argue that wealth taxes could extend the notion of ability to pay to help bear the costs of the crisis. [24]

The appeal of such a capital levy is that if implemented before avoidance is possible and there is a belief that it will not be repeated, it does not distort behavior and may be seen as fair by some.

There is a large amount of experience to draw on, such as levies widely adopted in Europe after World War I and in Germany and Japan after World War II. The Japanese effort was a success because it was imposed by the occupying American forces, minimizing the negative impact on the reputation of subsequent sovereign government. However, all other experiences proved a failure to achieve debt reduction because delays in the introduction gave time for extensive avoidance and capital flight – in turn spurring inflation.

Currently the scope for a wealth based capital levy to restore macro-financial stability appears limited. From a sample of fifteen Euro areas countries, the IMF calculates that a tax rate of about 10% on positive net household wealth would be needed to restore debt ratios to pre crisis levels. [25]

Politics and history

Those that argue against the economic efficiency of wealth taxes find the reason for their existence in politics and history. They argue that when a candidate looking for (re-)election meets voters who know little about the economic effects of taxes, then fiscal policy appealing to the feeling of solidarity and wish for equality promises to be a successful political strategy.

Regards history, it is posited that countries like the US and UK have been reluctant to impose a wealth tax because there is a widespread belief that wealth reflects past effort and ability. In the US, feudalism has never existed, and in the UK, secure private property rights evolved very early even under monarchic rule. On the other side, as in continental Europe where wealth taxes have been common, commentators point to a supposed prevailing belief that being wealthy is the result of favourable circumstances felt to be not very respectable. These include having political protection, being born into a dynasty or simply good luck. [26]

In April 2013 a group of reporters called the International Consortium of Investigative Journalists (ICIJ) shattered the long-held view that offshore bank secrecy was impenetrable. The group had received leaks detailing around 2.5 million individual bank accounts and then uploaded them to their website. This propelled a global wave of stories about the finances of high net worth individuals, including perceived tax evasion and avoidance. This not only prompted governments to take action but further stoked public debate around wealth taxes. [27] Most recently, in November 2017, a similar leak by the ICIJ dubbed The Paradise Papers occurred, highlighting damning cases of tax abuse and questionable business practices involving multinational companies and high net worth individuals. No doubt this will promote the wealth tax debate.

References

[1] International Monetary Fund – Fiscal Monitor October 2017, p2

[2] International Monetary Fund – Fiscal Monitor October 2017, p3

[3] A Wealth Tax Abandoned: The Role of the UK Treasury, Glennerster 2012, p1

[4] International Monetary Fund – Fiscal Monitor October 2013, p38

[5] International Monetary Fund – Fiscal Monitor October 2013, p26

[6] Wealth Tax in Europe in the Context of Possible Implementation in Romania – The Existing Wealth Tax and its Decline in Europe, Ristea and Trandafir 2010, p305

[7] http://www.economist.com/node/21564412

[8] http://www.worker-participation.eu/National-Industrial-Relations/Across-Europe/Trade-Unions2

[9] Scenarios and Distributional Factors of a Household Wealth Tax in Ireland, Lawless and Lynch 2016, p5

[10] International Monetary Fund – Fiscal Monitor October 2013, pvii

[11] Scenarios and Distributional Factors of a Household Wealth Tax in Ireland, Lawless and Lynch 2016, p7

[12] International Monetary Fund – Fiscal Monitor October 2013, p14

[13] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p825 – 830

[14] Scenarios and Distributional Factors of a Household Wealth Tax in Ireland, Lawless and Lynch 2016, p7

[15] Wealth Distribution and Taxation in EU Members, Iara 2015, p11

[16] https://newrepublic.com/article/117499/heres-what-we-know-about-thomas-pikettys-wealth-capital-tax

[17] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p822

[18] Wealth Distribution and Taxation in EU Members, Iara 2015, p9 – 10

[19] International Monetary Fund – Fiscal Monitor October 2013, p34

[20] International Monetary Fund – Fiscal Monitor October 2013, p39

[21] Wealth Distribution and Taxation in EU Members, Iara 2015, p10

[22] Taxing Wealth – What For? Schnellenbach 2012, p18

[23] https://newrepublic.com/article/117499/heres-what-we-know-about-thomas-pikettys-wealth-capital-tax

[24] Wealth Distribution and Taxation in EU Members, Iara 2015 p10

[25] International Monetary Fund – Fiscal Monitor October 2013, p49

[26] Taxing Wealth – What For? Schnellenbach 2012, p18

[27] Wealth Under the Spotlight, Ernst & Young 2015, p5

***

Wealth Taxes III: Problems

Introduction

This brief deals with the problems with wealth taxes and is broken into five sections: (1) Ways in which wealth taxes may be inequitable, (2) A heavy burden on the middle class, light on the rich, (3) The complexities of administration and high cost of collection, (4) Low revenue, and (5) Unintended consequences.

Ways in which wealth taxes may be inequitable

Wealth taxes are to some an intrusion on private property when compared to income taxes. With wealth taxes, the government has a claim against a taxpayer’s net assets, no matter whether the assets have generated an income or not. [1]

Narrowly defined wealth tax bases require higher tax rates to generate substantial revenue, reinforcing discrimination between asset types. [2] On the other hand, wider tax bases make it more difficult to prevent evasion, which in turn increases inequalities between taxpayers with different degrees of honesty. [3]

Consider two people with equal life spans, levels of starting wealth and continuing income, but different savings and asset disposal/transfer rates going forward. The person who saves more and disposes/transfers his/her assets more slowly will pay more wealth tax. [4] The person who does the opposite will be paying more VAT and other wealth-type taxes as discussed in the first brief. Thus an in depth cost benefit analysis will be required to try mitigate any inequities.

Some argue that the main benefit of holding wealth is insurance against shocks to human capital. If so, a wealth tax rate that doesn’t decrease with age discriminates against retired and older people who have much less human capital. [5]

Furthermore, the acquisition of wealth is a function of the 'life cycle,' i.e. the usual point of maximum net wealth is just as we retire: mortgages are paid off and pension savings is at its greatest. Thus net wealth taxes will have a disproportionate effect on senior citizens on the verge of retiring. [6]

Human capital is nearly impossible to tax, but excluding human capital from wealth taxes can be inequitable as the following scenario shows:

Consider two individuals Peter and Kate. Peter inherited his wealth in the form of bonds, consumes the interest payments and has no other income. Kate has no savings but has an excellent qualification and a job with a long term contract. Assuming the present value of Kate’s future pay equals the value of bonds held by Peter, a wealth tax on financial assets and not human capital discriminates against Peter who will not be able sustain the same level of consumption as Kate. [7]

Wealth taxes are double taxation when wealth consists of saved incomes that were previously subjected to income tax. Double taxation however is not unique to wealth tax as VAT is paid on goods and services out of taxed income.

A simple flat-rate wealth tax structure, i.e. non-progressive, discriminates against taxpayers at the lower end of the wealth scale who still need to build up wealth for savings and retirement. This feeds well into the next section. [8]

Heavy burden on the middle class, light on the rich

Surveys in the UK show that the middle class are most resistant to a wealth tax, because as one might expect, they have the strongest desire to leave as much of their limited wealth as possible to the next generation. [9]

The middle class tend to have most of their wealth tied up in an immobile and tangible asset, their home. The rich however have their home and other far more liquid and intangible assets. These additional assets owned by the rich are significantly more difficult for the authorities to tax, for reasons discussed later this brief, which has resulted in chronic tax avoidance by the rich globally.

Fast rising house prices can bring more middle class into the wealth tax net. A more middle class friendly wealth tax system would therefore require an exemption threshold that adjusts along with house prices.

House price revaluation is costly and will be borne more heavily by middle class taxpayers, especially those living in an area with few housing market transactions. [10]

What if lived in family homes were exempt from the wealth tax? This unfortunately would provide a strong incentive to borrow against other chargeable assets to invest in the home. It may also lead to older taxpayers who should be in sheltered accommodation choosing to stay home because of the tax break. [11]

As mentioned above, the rich are better equipped to take advantage of tax avoidance and even evasion opportunities that occur mostly though cross border transactions. For this to be reduced an international consensus on a wealth tax regime would need to be reached. Currently there is no agreement amongst the revenue authorities about the taxation of wealthy individuals. [12]

The lack of cooperation among countries in setting tax policies is fully intended and known as mercantilism: governmental regulation that promotes a nation's economy for the purpose of augmenting state power at the expense of rival national powers.

One careful estimate is that there is about US$4.5 trillion in unrecorded household assets located in tax havens. [13]

The effectiveness of a wealth tax thus rests largely upon effective limitations to tax shelters available to the rich, possible only if there was unfettered cooperation and information exchange between governments worldwide.

Lastly, due to the challenges and inefficiencies in taxing difficult to value or locate assets held by the rich, it has been suggested that some of these assets should be excluded from the wealth tax base. Such a partial approach however is plainly inequitable and might worsen wealth inequality instead of reducing it. [14]

The complexities of administration and high cost of collection

Wealth taxation requires regular asset valuations that impose additional costs on taxpayers and increases admin costs for the receiver of revenue.

Taxpayers will incur the costs of valuing his/her assets just to ascertain whether or not he/she is liable for wealth taxes. [15]

For any receiver of revenue, valuing assets within a taxpayer’s wealth portfolio is an expensive and difficult task. Furthermore, valuations are often speculative and easily manipulated, resulting in disagreements between the taxpayer and the receiver. This creates difficulties for both parties in planning ahead. To try and mitigate this, annual taxes could for example be charged on valuations done every five years.

Fortunately the cost of processing asset valuation information has been rapidly declining thanks to advances in information technology. [16]

Wealth taxes raise potential liquidity issues for taxpayers. The assets being taxed might not produce the income necessary to pay the tax and the owner will need to find funds elsewhere. If they cannot, he/she will have to sell part of or the entire asset, ultimately resulting in an erosion of equity.

Those arguing against the liquidity issue assume that a progressive wealth tax will sufficiently mitigate the problem because wealthier individuals are more likely to receive higher liquid incomes. It may be further mitigated, they say, by a deferral of the tax liability (to the moment of liquidation for example). [17]

If works of art have to be sold because of liquidity issues it could lead to a dispersal of national heritage. In France therefore works of art are exempt from wealth taxes. [18]

A 2015 study by the European Commission on Wealth Distribution and Taxation in EU member states found that wealth tax policy approaches tended to be piecemeal or incomplete. This, the study stated, obscured the wealth tax policy debate and challenged the introduction of wealth taxes. [19]

In order for the taxation of wealth to gain political support, the public will need to perceive the benefits of publicly provided goods financed by wealth taxes in mitigating socio-economic inequality. Public administration and tax-benefit systems that deliver both on efficiency and fairness are cornerstones of wealth taxation. Special fiscal mechanisms, such as earmarking wealth tax receipts to fund specific projects instead of plain redistributive spending, might also enhance the acceptance of wealth taxes. [20] Furthermore, because a system of taxing wealth has to operate over a person’s lifetime and is vulnerable to changes in government, to be effective there must be political consensus on how wealth is taxed. [21] It thus follows that if there is no political consensus, a tax payer who believes that wealth taxes will change with a change in government will try and delay declaring his/her wealth. [22] Finally, the tracking of ownership of mobile assets might be seen by some with suspicion for fears of coercive wealth levies. [23]

Globally, there is a lack of reliable household wealth distribution data as well as great difficulties in predicting behavioral responses to wealth taxes. These two factors mean that any analysis of the effects of changes in the taxation of wealth will be speculative and potentially dangerous if acted upon. [24]

Low revenue

Historically, revenue from net wealth taxes has been low in countries applying them, ranging from 0.07% to 5% of total national revenue [25]. In the South African context, Judge Dennis Davis of the Davis Tax Commission is quoted as saying “I would be very surprised if a wealth tax brought in more than R5 billion a year.” [26] This would come to 0.44% of the R1.144 trillion total revenue for the 2016/17 tax year.

Evasion and difficulties of asset valuation have been considered key in reducing the revenue generating capacity of wealth taxes. [27] Thus zero-tax allowance thresholds have been suggested to lighten administration. However, if these thresholds are too high it will jeopardize the production of revenue. [28]

Due to the moderate revenue it generates, wealth taxes can contribute only minimally to reducing inequality. The Swedish government, which abolished wealth taxes in 2007, said they found their performance disappointing in terms of both revenue and perceived impact on inequality. [29]

In 2010 the Institute of Fiscal Studies in the UK released a report on the then current system of taxing wealth in the UK and the potential for the introducing a net wealth tax. The following is an extract from the study:

Such a major change in the tax system needs to be justified by a sufficient margin to outweigh the costs of change, and it is far from clear that the advantages of a wealth tax are sufficiently great to justify the risk of such a change. For example, the yield of wealth taxes in countries such as France has not been significant. [30]

Unintended consequences

A 2008 study titled The Economic Consequences of the French Wealth Tax, by Professor Eric Pichet of Kedge Business School, found that France loses around 5 billion Euros in tax revenue a year because of people leaving to avoid the wealth tax. Pichet goes further to say this capital flight could cost at least 0.2% of annual GDP due to a decrease in investments.

Since 2000, France has experienced a net outflow of around 60 000 millionaires. Vincent Lazimi, a partner at law firm Vaslin Associés, says “There has been an acceleration of departures from France due to the unstable nature of the policy (wealth tax).” [31]

This all leads well into the following paragraphs on wealth taxation’s effect on tax evasion, savings, investment, entrepreneurship and ultimately growth.

Only net wealth is taxed, and because of this taxpayers will be incentivized to avoid the tax by borrowing against his/her assets and investing the funds in a jurisdiction or asset that is exempt from wealth tax. [32]

In Switzerland where wealth taxes still exist, a group of economists recently found that wealth taxes there substantially reduced reported wealth holdings as taxpayers aimed to get their wealth to just below threshold levels at which they will not be liable for wealth taxes. [33]

To limit evasion and avoidance, an international consensus on wealth taxation would need to be reached, an extremely difficult task. Technology too has made it easier for funds to be shifted at low cost around the globe, and while this has contributed to tax evasion, the World Economic Forum argues that it may also help fight it if authorities have access to the right data, technology and laws are adapted to the new realities. The recent OECD and G20 initiative on base erosion and profit sharing, the WEF says, is a welcome first step. [34]

The 2015 European Commission report on Wealth Distribution and Taxation in EU Members as well as the 2016 German Institute for Economic Research report on Inheritance Tax and Wealth Tax in Germany both conceded that the introduction of a wealth tax could result in capital flight. In fact, when net wealth taxation was abolished in Ireland and Holland, the most important reason given by those governments was capital flight. [35]

Savings and investment decisions may become distorted as a result of wealth tax.

Savings could decrease as taxpayers are incentivized to substitute future consumption with present consumption, causing efficiency to suffer. Also, the allocation of savings between different investments may be distorted if they are subject to different taxes. [36]

It may not be obvious at first, but if a tax payer’s net assets earn a return of 3%, a 1% wealth tax is a 33% tax on that return. [37]

Wealth tax also increase the required rate of return on investments. Consider a potential investment with a required return of 5% and wealth tax at 1%. To make the investment viable, the equilibrium required return then becomes 6.05%. This is a 21% increase in the required return due to the wealth tax. [38]

Individuals might become more discouraged than before from making risky investments because wealth taxes automatically increases investment risk. Under income tax, a taxpayer can write off investment losses against gains when calculating taxes owed. Thus government indirectly shares in the investment risk. This however doesn’t happen under wealth taxes. When an investment in a wealth tax system experiences a loss, government is unaffected because the taxpayer is still required to pay the full amount, thereby exacerbating the loss. [39]

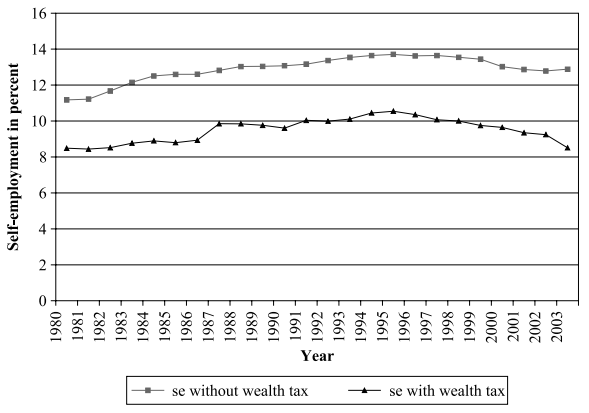

Finally and empirically, wealth taxes have a negative impact on entrepreneurship. The following is taken from a 2008 study, The Wealth Tax and Entrepreneurial Activity by Lund University’s Asa Hansson:

Data from twenty-two OECD countries indicates that countries that do not tax wealth have systematically higher self-employment than countries that do tax individual wealth. Average self-employment, indeed, was 24 per cent higher in countries without a wealth tax than in countries that taxed wealth over the time period 1980 to 2003.

Average Self-employment Rates in Wealth and Non-wealth Tax Countries, Respectively, over 1980 to 2003

Hansson found the reasons for the above to be:

1. Taxing wealth reduced the amount start-up capital available.

2. The major motivator for entrepreneurs is after-tax returns, which is reduced by a wealth tax.

By Charles Collocott, Researcher, HSF, 4 April 2018

References

[1] Taxing Wealth – What For? Schnellenbach 2012, p17

[2] Taxing Wealth – What For? Schnellenbach 2012, p9

[3] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p786

[4] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p750

[5] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p833

[6] The Problem with a Wealth tax, Wall Street Journal, January 11, 2012

[7] Taxing Wealth – What For? Schnellenbach 2012, p13

[8] Wealth Distribution and Taxation in EU Members, Iara 2015, p11

[9] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p749

[10] Wealth Distribution and Taxation in EU Members, Iara 2015, p9 – 10

[11] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p775

[12] Wealth under the Spotlight, Ernst & Young 2015, p4

[13] International Monetary Fund – Fiscal Monitor October 2013, p40

[14] Wealth Distribution and Taxation in EU Members, Iara 2015, p13 – 14

[15] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p784

[16] Wealth Distribution and Taxation in EU Members, Iara 2015, p20

[17] Wealth Distribution and Taxation in EU Members, Iara 2015, p20

[18] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p783

[19] Wealth Distribution and Taxation in EU Members, Iara 2015, p19

[20] Wealth Distribution and Taxation in EU Members, Iara 2015, p20

[21] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p742

[22] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p810

[23] Wealth Distribution and Taxation in EU Members, Iara 2015, 2015, p20

[24] Wealth Distribution and Taxation in EU Members, Iara 2015, 2015, p21

[25] http://www.dw.com/en/would-a-wealth-tax-be-effective/a-16282381

[26] https://www.moneyweb.co.za/mymoney/moneyweb-tax/what-a-wealth-tax-could-look-like/

[27] Wealth Distribution and Taxation in EU Members, Iara 2015, 2015, p9

[28] Wealth Distribution and Taxation in EU Members, Iara 2015, 2015, p14

[29] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p833

[30] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p787

[31] https://www.ft.com/content/19feb16a-1aaf-11e7-a266-12672483791a

[32] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p784

[33] Taxing Wealth: Evidence from Switzerland, Brülhart, Gruber, Krapf, Schmidheiny 2016, p4

[34] International Monetary Fund – Fiscal Monitor October 2017, p28

[35] Taxation of Wealth and Wealth Transfer, Broadway, Chamberlain and Emmerson 2010, p787

[36] Taxing Wealth – What For? Schnellenbach 2012, p8

[37] International Monetary Fund – Fiscal Monitor October 2013, p39

[38] Taxing Wealth – What For? Schnellenbach 2012, p6

[39] Taxing Wealth – What For? Schnellenbach 2012, p20