Over a period of several years I penned a number of economic commentaries on various websites who would have me. The general thread running through these columns was a warning about what I called a “financial tsunami” heading our way. I thought, naively, that by warning about this financial firestorm heading our way, I will be thanked. Instead, apart from a couple of reluctant “thank you’s” I seemed to have earned the moniker of being negative, unpatriotic and ill-informed.

As far back as 2012 I started sensing a slight shift, almost imperceptible, in the underlying economic mood which did not bode well.

To me the first signs of this tsunami was faintly visible far out at sea but it seemed to be mostly ignored by professional economists and analysts on shore.

My “tsunami alerts” had the following sequence: The first one was the collapse in the global commodity cycle in 2012/13 which saw prices for the stuff we dig out of the ground and sell overseas tumble quite significantly. It’s the one thing I learnt from my economic studies many decades ago. We are a commodity -producing country and if this cycle turns negative, as it did, get out of the way.

This was soon thereafter followed by downgrades by the global ratings agencies from 2012 onwards, Moody’s originally, and eventually to junk by S&P Global Ratings and Fitch in December 2017 after former president Jacob Zuma fired Pravin Gordhan as finance minister while he was on his way to a global investment conference in London to attract foreign investments.

While Moody’s started the current trend of downgrades, ironically, it today remains the only major credit ratings agency which has not downgraded SA fully to junk. We hang on my the thinnest of finger-nails.

The global investment community did not take kindly to this cynical turn of events and started withdrawing capital from the SA equity and bond market. So far the selling- down of SA assets since the beginning of 2015 is close to R500 billion, more than the massive sell-off during the Great Financial Crisis of 2008. This selling down does not attract front-page coverage, as it should, as it has been staggered over several months and years.

The selling continues unabated and the latest numbers of August 2019 suggest a further disinvestment of R68 billion from our bond and equity market.

Other tsunami alerts were the financial damage wreaked by Zuma and his programme of State Capture, a collapse of law and order and a general rise of civil obedience and lawlessness. At first these incidences were localized but it has now spread like a massive veld-fire and is almost everywhere. South Africa today is very close to a state of widespread anarchy and a general breakdown of law and order.

Today a wide range of columnists have joined me in warning about the financial precipice SA is standing on.

There were a number of early-warning signals which alarmed me and I acted on them in my own personal capacity and I also tried to advise as many as I could in a professional one as well. I sold out my share portfolio on the JSE, withdraw money from my pension fund and sold some residential properties in order to build up cash and create an offshore portfolio. I was also not shy about these steps I was taking. On every platform, including radio, TV and in press interviews, I repeated these views of mine.

And as time went on these alarm bells were ringing ever-more strongly, but it seemed as if I was the only one hearing them.

Many people looked askew at me, often predictably so, as the general consensus was that everything was hunky-dory.

One article in particular, which was published on Moneyweb October 2016, earned a stinging rebuke from one Dr. Roelof Botha, consulting economist at the time to GIBBS business school, who called me “cynical”, “ill-informed” and possibly even stupid. “Talk of a financial tsunami misplaced”, was the screaming headline they used a week later in reply to my original article.

Botha said the downturn was to be short-lived, talks of a downgrade to junk misplaced and that a growth rate of 4% per annum was soon to be ours. This, ladies and gentlemen, was from one of our top economists having won the Economist of the Year-Award once or twice. Since then our growth rate has battled to exceed 1% per annum and this year could be as low as 0,5% for the year.

This view of normality and future stability was reinforced by the repeated statements by both government and the private sector that SA’s economy was on a sound footing and that any downward deviation from the long-term pattern growth patterns would be mild and temporary.

I spent a great deal of time over the past week on Google trying to find any other economic commentator issuing similar warnings. The warnings were there, but they tended to be from economists linked to or employed by smaller, more independent companies. One can include people like Mike Schussler (economists.co.za), Dr Dawie Roodt from the Efficient Group and also Russel Lamberti amongst this small group who did not share the general optimistic view of our economic future.

The bulk of the economic forecasts during the period 2014-2019 gave very little hint of the financial tsunami heading our way. In fact, most economic forecasts had a predictable pattern to them over these 5 years which I analyzed.

At the beginning of every new year the consensus forecasts made in the Economist of the Year-competition run annually by the newspapers in the Naspers-stable, was generally upbeat and positive about the year ahead. But then, as the year progressed, the forecasts were adjusted downwards in terms of growth rates, unemployment rates, ZAR/dollar exchange rates and a host of other economic variables. It appeared to me that these economists were rather conservative in their longer-term outlook and/or under strict instructions from higher up not to rock the boat.

Obviously I can never prove it, but I reckon (and so does Dr. Frans Cronje of the SA Institute of Race Relations) that our formal economists, attached to banks or asset managers, have to toe a very strict party line. Don’t criticize government and don’t tell the truth about the economy. Step out of line and you are in the firing line.

So the bottom line is that if you had used these forecasts made by our mainstream economists you would have not acted or taken steps to avoid the tsunami and most probably would have (a) bought more residential property, (b) bought more shares on the JSE and (c) perhaps even taken on more debt to fund an expansion of your business.

The forecasts made annually by Treasury over this period was also hopelessly over-optimistic, to such an extent that each of the past five annual budgets have gotten the forecast for revenue for the year ahead wrong and each forecast had to be very rapidly adjusted downward. This year was no exception and almost two months into the financial year we are heading towards an even-larger under-recovery of revenue for the current fiscal year. This year, I feel, the under-recovery is going to be particularly bad as a slowdown in retail sales, property transfers and an overall weak economy, much worse than expected, take their toll of government revenue. All will be revealed during the Medium Term Budget Statement next month.

The full-blown impact of this financial catastrophe is to be seen everywhere. Record unemployment, stagnant economic growth, government debt levels rocketing from 25% of GDP in 2009 to an expected 60% by the end of this year. There are today more people on social grants (17,3m) than those who earn a living. The residential property market has now moved sideways for 11 years and in reals terms is down 23% when inflation is factored in. The JSE has just had its worst 5-period on record and the rand has collapsed from R6,80 in 2012 to around R15 today. South Africans are infinitely poorer today than 5 and ten years ago and the number of so-called High Net Worth Individuals (people with more than $1m in liquid assets) have sharply reduced from 48 000 to around 43 000 today, according to New World Wealth.

Earnings of JSE listed companies have tumbled from around 11% of GDP in 2017 to about 5% end of 2018. If all companies in SA –listed and unlisted--were treated as one company, then this company did not make a profit last year.

Golf courses are empty on a Saturday morning as are bowling clubs and many suburban malls. Many of our small to medium sized towns are wastelands today with no or very little money spent on infrastructure and/or maintenance.

Confidence amongst both consumers and business people is at an all-time low. The ANC’s policies of Expropriation Without Compensation (EWC) and now also the suggestion of prescribed assets on pension funds and other financial assets has shattered whatever confidence was left. But don’t expect to have been warned about this by the mainstream economists and asset managers.

There are heightened expectations that Moody’s will revise its outlook on SA from stable to negative when it publishes its next report on 1 November, which could see the country lose its final investment grade soon after.

A downgrade would trigger mass portfolio investment outflows as investors not mandated to hold sub investment grade bonds will have to dump them. While S&P Global Ratings and Fitch Ratings downgraded SA to junk status in 2017, Moody’s has given the country the benefit of the doubt. SA had a reprieve from Moody’s at the end of March when it did not make a pronouncement on the country. However, SA’s domestic fiscal position has weakened significantly, particularly after additional bailouts to state-owned companies.

The asset managers themselves, particularly the big ones, have also not covered themselves in glory as far as their forecasts have concerned, especially when it came to the expected performance of the JSE versus the rest of the world markets.

For the last three to four years have I sat through numerous investment presentations by the Big Ones (Old Mutual, Coronation, Allan Gray, PSG et al), confidently predicting an imminent resurgence of the JSE, based on, amongst other things relative valuations. And as most investors with local holdings know, the past 5 years has been a write off for most local equity funds, particularly the past 3 years.

Earlier this year Old Mutual went on a roadshow confidently proclaiming that the JSE will be one of the best investment markets in the world over the next five years. It was so convincing that it made the front-page of the Business Day, our foremost publisher of financial news in SA. So far, nothing has come of this forecast and is the JSE still one of the laggards of global stock markets.

Last week research company Corion reported that the average returns of general equity funds on the JSE, at an average growth of 1,7% per annum, was the lowest on record. I expected this to be front-page news of financial media and being discussed on radio and TV, but I could hardly find any mention of this poor performance anywhere.

All I could find were articles by asset managers urging South Africans to save more in order to avoid a dreary retirement! Into the same investments that have not beaten the inflation rate now for 6 years. Hardly a word about the economic destruction caused by the ANC’s economic policies, or the effect of State Capture or the potential impact of EWC. It’s like these nasty things don’t exist in the mind of the large asset managers.

Here’s where it gets interesting. It surprises most people when I tell them fund managers are not licensed to give investment advice. That’s why all investment presentations end with a very small disclaimer that any information provided is not financial advice and that the speaker/company represented it not liable for investment losses. Very few notice these disclaimers and often people act on these forecasts, especially if these presentations are reported in the media.

The media too, plays a role in this pretense of normality, especially the financial media. The media too is a victim of this financial tsunami and will often not dare criticize the large asset managers on their conduct for fear of losing whatever little advertising revenue they still have.

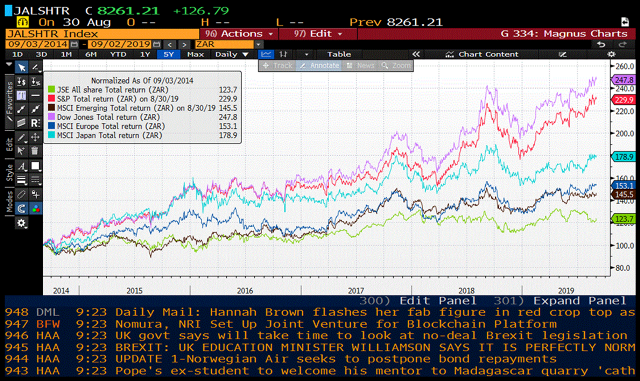

Nowadays hardly a day goes by without some media outlet not reporting on the seemingly compelling value on offer by the JSE, yet what is lacking is a comparative analysis on how the JSE has performed over the past 5 years. The JSE has been one of the worst performing major stock markets in the world over the period, and as discussed above, has not beaten the inflation rate over 5 years and soon over 7 years.

The same goes for our country’s retirement fund returns which, too, have not beaten inflation over 5 years. I have seen investment returns from some of SA’s large investment companies where their returns on retirement annuities and preservation funds have been zero over 5 years.

SA’s retirement industry is controlled by Regulation 28 of the Pensions Act which limits the percentage exposure funds may have to various asset classes, including a restriction of only 30% to offshore funds.

As a consequence two things have happened (which partially explains why most people will have a dreary retirement)” local investors have missed out on one of the most explosive booms on the US markets in history, and (b) they have been forced to invest the bulk of their assets in a severely lagging market. The end result: a dismal retirement.

And to make matters worse, government now has its eyes on the R4 trillion pension pot and is considering introducing prescribed assets, which will decimate growth even more.

See here charts of how the JSE has performed over 5 years in rand terms.

Local investment companies are not fighting each other for market share as much as they are fighting against the giant offshore investment companies for the share in the global investment arena. There is very little local appetite for direct investing on the JSE at the moment. Most of the flows of new money has been into high income funds, fixed deposits with banks and offshore funds.

I predict that unless there is a profound and fundamental change of the economic policies of the ruling ANC, the outward flow of money will continue with most high net worth investors eventually ending with a great deal of their wealth offshore. As it is, there is currently a veritable flood of money flowing out of the country in order to diversify and to even circumvent the potential re-introduction of exchange controls.

For many the tsunami has already hit and has left in its wake financial destruction, plunging net asset values—particularly in dollar terms—and a desperate search for inflation-beating investments.

A whole generation of South African baby boomers is bearing down on retirement with (a) residential property in a funk and (b) retirement pots severally damaged by Reg 28 and exchange controls. Most retirement projections, I would suggest, are out by 20-30% leaving already-underfunded retirements even more underfunded. In short: a dreary retirement awaits all but the very rich and the very smart who externalized a great deal of their assets timeously.

*Magnus Heystek is investment strategist at Brenthurst Wealth